By staying up to date with your bookkeeping throughout the year, you can help alleviate some of the stress that comes with filing your taxes. Let us walk you through everything you need to know about the basics of bookkeeping. The last of them was a direct-to-consumer how many years can you file back taxes health tech startup focused on sperm freezing called Sppare.me, which he scaled to a “high seven figures” in sales, he said. The hard-won success is what gave Pinchevski the inspiration to tap his accounting expertise to start Finaloop, he added.

- In most of the countries, the accounting period is the financial year which starts from 1st April and ends on 31st March of every year.

- This more advanced process is ideal for enterprises with accrued expenses.

- To make it even easier, bookkeepers often group transactions into categories.

- Financial institutions, investors, and the government need accurate bookkeeping accounting to make better lending and investing decisions.

What Is Bookkeeping? Definition, Tasks, Terms to Know

As you might expect from that pedigree, they have been fiscally prudent when it comes to growth. And when you’re ready for more podcasts, articles, case studies, books, and videos with the world’s top business and management experts, find it all at HBR.org. “It will be unsettling for a time and uncomfortable adjustments will be made. I too, will be making new shopping plans for my books.” The New York Times reported earlier this week that Costco plans to stop regularly selling books year-round starting in January 2025, citing four anonymous publishing executives.

The difference between bookkeeping and accounting

In 2012, she started Pocket Protector Bookkeeping, a virtual bookkeeping and managerial accounting service for small businesses. In this episode, you’ll learn how the company created and sustained a culture of innovation that challenged conventional assumptions about management and process. You’ll also learn why leaders there intentionally chose not to rely on their past experience and intuition as they designed new digital experiences.

Bookkeeper Duties

It’s a great choice for anyone who needs a simple bookkeeping solution that will allow them to manage their expenses and income quickly. However, it’s important to note that your bookkeeper won’t be the only person working on your business finances. So you’ll want to understand which tasks your bookkeeper is and isn’t responsible for handling. Your reports will look different depending on which you decide to use.

Single-entry accounting records all of your transactions once, either as an expense or as income. This method is straightforward and suitable for smaller businesses that don’t have significant inventory or equipment involved in their finances. It doesn’t track the value of your business’s assets and liabilities as well as double-entry accounting does, though.

In particular, the big four firms of Ernst & Young, Deloitte, KPMG, and PricewaterhouseCoopers offer larger salaries than mid-size and small firms. Depending on the city, you can expect to earn between $40,000 and $60,000 your first year as a Big Four accountant. While the companies do not publish salaries on their websites, the benefits can be https://www.quickbooks-payroll.org/ a large draw. For example, KPMG offers employees up to 25 days of paid vacation time, telecommuting opportunities, and a robust health insurance package. As an accountant, you may have to crunch numbers, but those are not the only skills needed. It is important to possess sharp logic skills and big-picture problem-solving abilities, as well.

While there are certain similarities and overlaps between the two, there are distinctions that set these two roles apart. Bookkeepers don’t necessarily need higher education in order to work in their field while accountants can be more specialized in their training. Because bookkeepers tend to work for smaller https://www.personal-accounting.org/modified-internal-rate-of-return/ companies, they may not be paid as much as accountants. Knowing the differences between the two can help people find their niche in the industry and can give guidance to companies on who to hire for their needs. Rather your business is large or small, you need an understanding of your accounting needs.

Under single-entry, journal entries are recorded once, as either an expense or income. Assets and liabilities (like inventory, equipment and loans) are tracked separately. If you’re just starting out, are doing your books on your own and are still in the hobby stage, single-entry is probably right for you. If you wait until the end of the year to reconcile or get your financial transactions in order, you won’t know if you or your bank made a mistake until you’re buried in paperwork at tax time.

At least one debit is made to one account, and at least one credit is made to another account. Bookkeeping is the process of keeping track of every financial transaction made by a business—from the opening of the firm to the closing of the firm. Depending on the type of accounting system used by the business, each financial transaction is recorded based on supporting documentation. That documentation may be a receipt, an invoice, a purchase order, or some similar type of financial record showing that the transaction took place. Bookkeeping traditionally refers to the day-to-day upkeep of a business’s financial records. Bookkeepers used to simply gather and quality-check the information from which accounts were prepared.

There are critical differences in job growth and salaries between the two. Growth for accountants and auditors is expected to continue for the next several years. The Bureau of Labor Statistics (BLS) expects 6% job growth in this field from 2021 to 2031. To better understand these concepts and how to apply them, take bookkeeping courses that will allow you to practice them.

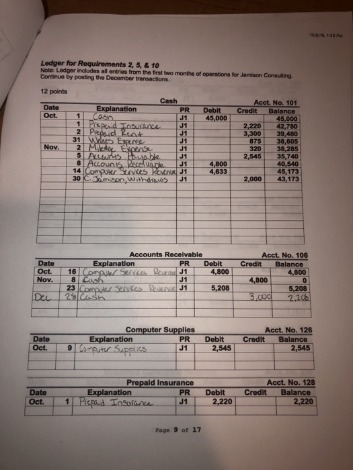

As we’ll learn, it is imperative that the ledger is balanced, so keeping an accurate journal is a good habit to keep. In the normal course of business, a document is produced each time a transaction occurs. Bookkeeping first involves recording the details of all of these source documents into multi-column journals (also known as books of first entry or daybooks). For example, all credit sales are recorded in the sales journal; all cash payments are recorded in the cash payments journal. Most individuals who balance their check-book each month are using such a system, and most personal-finance software follows this approach. Transactions include purchases, sales, receipts and payments by an individual person or an organization/corporation.

Leave a Reply